InMode Ltd. ($INMD)

A CEO Take Private Special Sit with potential bidding war.

TLDR

Ok, here’s a new one for you deal junkies after the wknd. I've seen very little chatter about it bar a few posts on Twitter. At first glance, this is just another CEO proposing to take his company, InMode, private for $16.20 a share, a 20% premium. But, if you look a little closer, it’s one of the more cheeky (read: nonsense) attempts I have seen in a while. That doesn’t mean it won’t succeed, though, the market was not pricing it like a done deal.

Steel Partners got the ball rolling in Jan with an $18 bid, but for just 51% of the company. The board was forced to act, but quickly ended the process without sharing much, other than the bids were inadequate (said to be between $16/17). That’s when CEO & co-founder Moshe Mizrahy swooped in with a.. lets say interesting proposal for $16.20, (below the previously rejected bids). Two activists (Steel Partners & Doma Perpetual) own ~8.5% of the company & aren’t happy about the CEO’s bid or the process. In fact they say he heavily influenced the board to reject the previous bids.

Now late last week - one has just come over the top ! It’s a fun one.. grab a coffee… or a beer & lets dig in..

The Company

I confess, I knew very little about this subject - so I would like to thank my editor (read: lovely wife!) for the background. InMode is an Israeli based medical device company that sells products used for energy /radio frequency based treatments like body or face contouring, aesthetic treatments & women’s wellness - like skin rejuvenation, tightening, fat removal etc. Marketed as a range of non or minimally invasive surgical medical treatments. Basically alternatives to proper surgeries. InMode’s customers are plastic & facial surgeons, aesthetic surgeons, dermatologists & OB/GYN’s. Their 285 sales reps sell their products direct in the US & additionally they sell through 73 distributors in over 101 countries. International sales account for 46% of total revenue. (38% in 2024). Essentially, the pitch is surgical-grade results (w/ small or no incisions) under local anesthetics while significantly minimizing risks of scarring, downtime, pain & other complications that would typically accompany going under the knife. No need for general anesthetics, less risk to the patient & most importantly it’s cheaper.

What I find particularly interesting is the capex spend. It’s much lower than I would have expected. Capex is predominantly made up of the initial buy of the molds to build the machines. From what I can gather, that’s because manufacturing is primarily outsourced to three subcontractors located in Israel. Two are identified: Flextronics (Israel) Ltd., or Flex, and (BY) Medimor Ltd., or Medimor. InMode has a 12% stake in Medimor. We’ll come back to this later..

Results / Financials

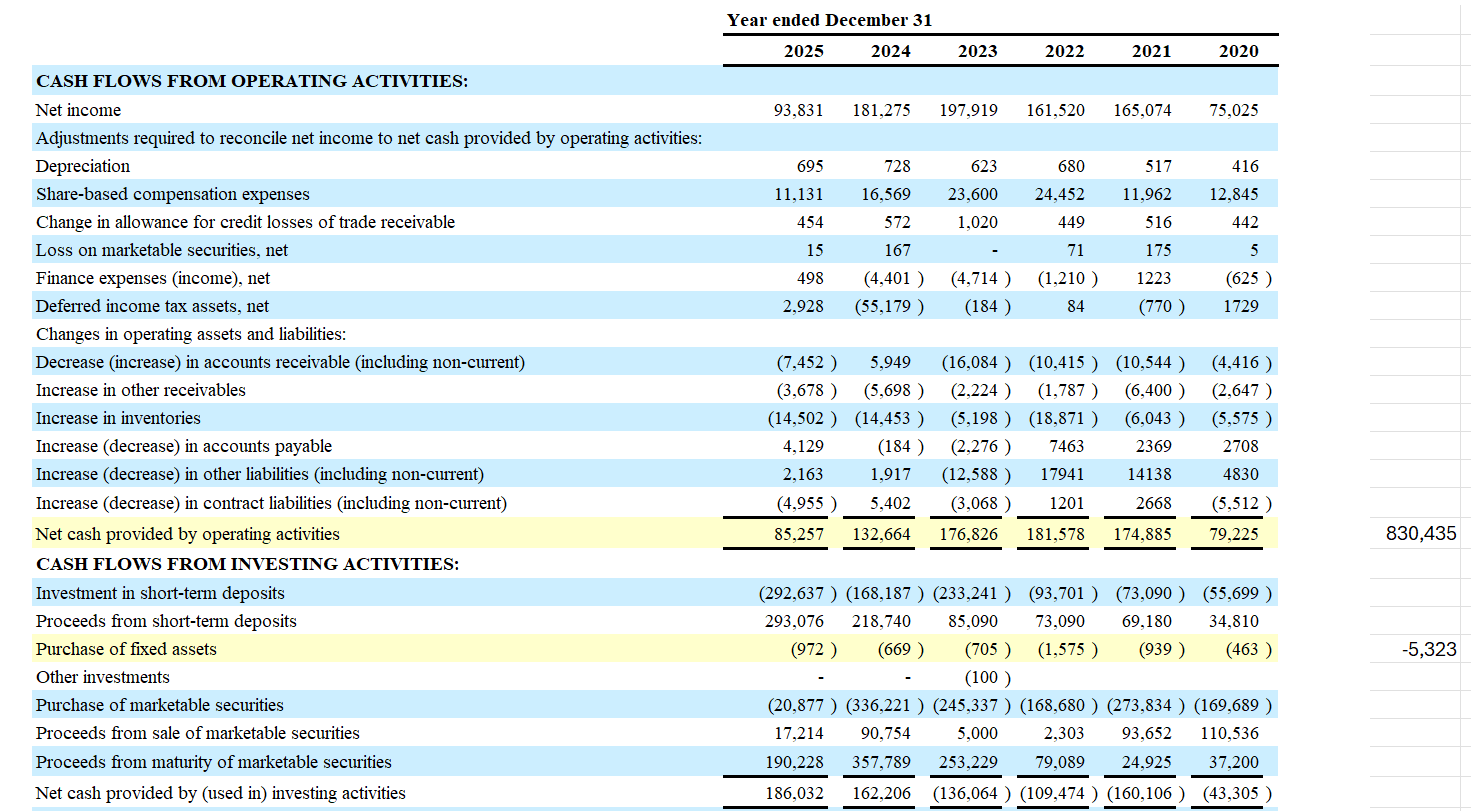

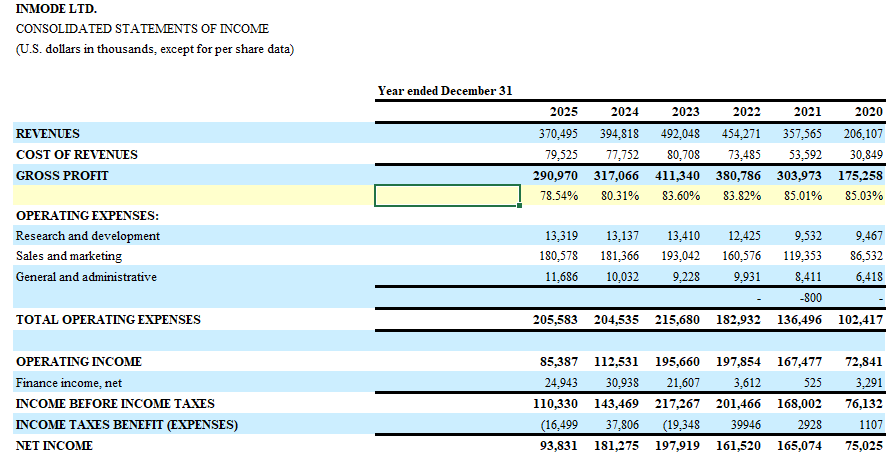

InMode had a few years of incredible growth as the Covid hangover boosted sales 75% in 2021 & 25% in 2022. Since then, we’ve seen a gradual decline in revenue & with it, free cash flow. Like many businesses during Covid, revenue was pulled forward & then subsequently declined. I think the recent decline is because buyers stocked up post Covid & sales tapered off after as a result. But unlike many businesses, InMode didn’t lever up at the wrong time assuming demand would continue to explode. So, this may prove to me a somewhat normal level of revenue as I don’t see the business going away - both surgical & non surgical treatments increased ~40% since 2020. Granted, that was likely an unnatural bottom (lol, excuse the pun !) - but I’m very confident that the aesthetic space will continue to grow & InMode will have it’s slice. The business generates lots of cash because capex is so low, gross margins are so high & there’s no debt to eat away at it. Revenue should stabilize & this will continue to be a cash machine. I think the CEO knows this & wants it for himself.

Most importantly to the thesis here is that the company has a bunch of cash on it balance sheet ($537m to be exact) & no debt. We’ll come back to this later too.

So, how did we get here ?

In Jan 26, Steel Partners published a press release making public an $18 offer for 51% of the company. Clearly they had been trying to engage management but to no avail.

Over the past several months, we have made multiple attempts to meet with the Company to discuss ideas for creating shareholder value. We have also recently attempted to engage in a private dialogue with InMode’s leadership around our attractive proposal, but have so far been rebuffed. Therefore, we believe it is imperative that you, the Company’s true owners, are made aware of this opportunity.1

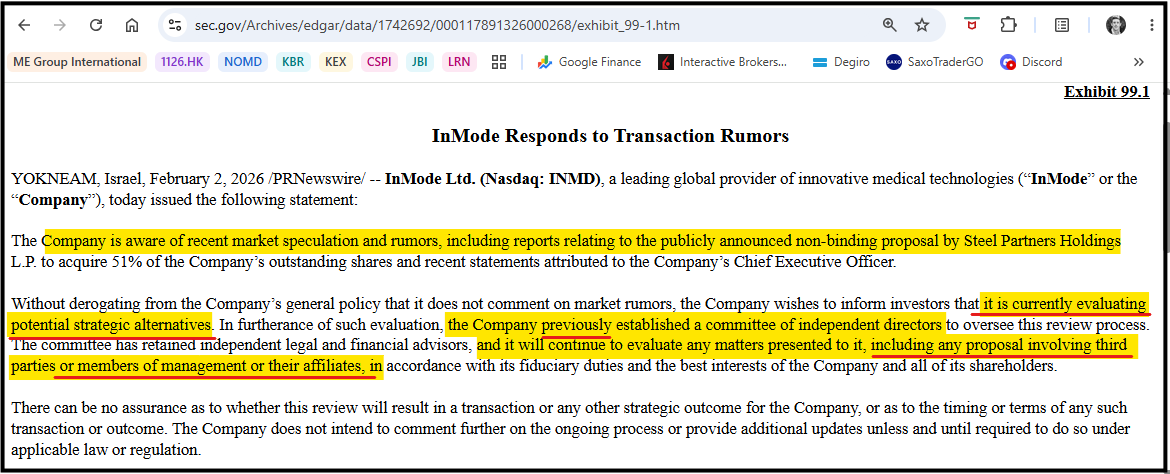

This forced the boards hand. Feb 2nd, InMode filed an 8-k & announced they were evaluating potential strategic alternatives, established a committee to oversee the process & retained legal & financial advisors. What was interesting to me at least was the wording - it was all past tense ! And, they snuck in the fact that they were already considering proposals from management !2

They also mentioned “and recent statements attributed to the Company’s Chief Executive Officer.” This looks to be a reference to the CEO;’s comments about Keeping InMode Israeli.3

Initially the article (in the Globes) reads like the CEO leaning hard on the company’s Israeli roots in what looks like a attempt to solidify support - but quickly turns into a rant about not having full control, a finger pointing exercise & a clear desire to take the company private.

The Doma fund’s belligerency, Mizrahy says, affected the InMode board. “It takes time but in the end it penetrates. The desire to go back to being a privately-held company arises from, among other things, the desire to get them off our backs. Running the company has become unpleasant.”

Feb 10th, on the Q4, 2025 earnings call the CEO took a pop against Steel Partners that dismissed the $18 a share offer saying..

We do not have 51% of the company to sell. So the only way to buy 51% of InMode is to do a tender offer, hire a bank, put some money in an escrow account and offer it to the public, not to the CEO. I don’t have 51% to sell and give them. But they didn’t do it. They just sent a letter to me and to the Board of Directors.

Feb 23rd - Just three weeks later the board killed the process.4

Following a careful review of the final proposals received in connection with the potential transaction, the Committee has concluded that none of the final proposals is adequate and in the best interests of the Company and its shareholders. Accordingly, the Committee has determined to discontinue the process at this time.

With the process dead, the stock proceeded to fall from ~$15 to the high $12’s over the following days.

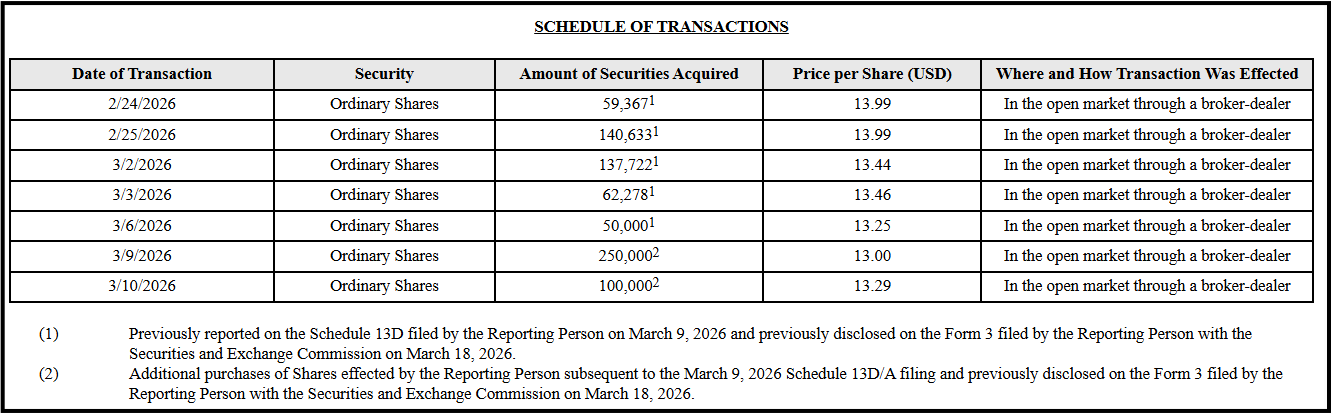

April 9th - The CEO filed a 13D revealing that as it sank, he bought 800,000 shares in the open market ! 4,299,226.00 / 7.06 %5

The very same day, Michael Kreindel, the firms co-founder & CTO filed a 13D. He had never previously filed a 13D. He owns 3,114,762 shares / 5.11 % of the company. 6

Take Private Proposal

June 24th - the CEO, Moshe Mizrahy updated his 13D & announced that M.N. Business Strategy (the buyer group) delivered a letter to the board prosing to take the company private for $16.20 a share.7 The buyer group is comprised of Moshe Mizrahy, the CEO & co-founder, Jeffrey Royer, who owns Medimor Ltd - InMode’s largest supplier ! & Bedo Eghiayan, & Michael Avedissian, who together own Wigmore Medical; InMode’s largest distributor ! Also, Meir Shamir, a prominent businessman & likely financial backer. Interestingly, Kreindel the CTO is not mentioned in the filing. What strikes me immediately is that the group is not your typical PE buyer but they likely know the business intimately.

The proposal is almost trying to make it sound like its already a done-deal. Note the language used - “binding proposal”. I very much doubt this is a typo, though its possible as there are a few. It just reads to me like there’s nothing left for the board to do bar approve it. Some excerpts below.8

M.N. Business Strategy, Ltd. hereby submits this binding proposal to acquire all of the issued and outstanding ordinary shares of InMode Ltd. that are not already owned, directly or indirectly, by the Buyer and its affiliates.

We confirm that we have completed all due diligence we deem necessary

We are prepared to proceed on an expedited basis and to coordinate with the Company to prepared and execute definitive documentation for the Transaction promptly following the acceptance of this Proposal.

We confirm that all internal approvals required for submission of this Proposal and to proceed to signing and closing have been obtained.

We look forward to hearing from you and completing the Transaction in a timely manner.

This Proposal shall remain open for acceptance until July 15, 2026, after which time it shall automatically expire, unless extended in writing by the Buyer.

Purchase Price & Valuation

The mental gymnastics needed to get anywhere near $16.20 is truly extraordinary.

First of all they use an expected EBITA figure of $65m !! Given the company guided for income from operations to be $75m at the midpoint - this seems like the group chipped off $10m just for kicks ! EBITA should be above this, not below gents.

Next, they’ve applied a 2.6x multiple because some of their competitors have filed for bankruptcy - which is hardly relevant & so settled on one company. They’ve ignored InMode’s market leading margins, ignored transaction multiples / precedent transactions & ignore AbbVie. Look, AbbVie is probably the wrong comp here too. It’s behemoth - but it is mentioned in the 20-F competition section & the proposal did not want to mention AbbVie as this was not convenient.

The buyout group also points to analyst targets as additional foundation of the bid. Unfortunately analysts price targets don’t account for control premiums. Sigh….

Finally, they’ve taken a haircut to the cash ! They’re telling us that they'd pay 25% div withholding - which of course, they don’t have to do. This nonsense is supposed to shrink the equity value further & reduce the amount they would have to pay. They’re also saying net cash was $489m - not $537.2 as of Q1. That’s another $48m poof ! The very cash that will be used to buy the company !!

Doma Perpetual Capital - ~3m shares / 4.6%

June 26th, two days later Doma Perpetual came out publicly against the deal & raised serious concerns about the obvious conflicts & governance. Doma argued that management are responsible for the poor share price performance while now benefitting from it. They called the $16.20 proposal conflicted & said they would vote against it. 9

Doma had already publicly voiced their concerns back in 2025 after getting nowhere with management. They highlighted the CEO’s negative public comments & partly attributed the declining stock price to them. They also called for the removal of the CEO.

Steel Partners - ~1.7m shares / 3%

June 30th. After the CEO’s take private proposal Steel Partners, in a press release slammed the CEO & Board. They highlighted the CEO’s public comments expressing a pessimistic view of the company’s performance - that it was designed to condition the market for his group’s low-ball bid. The letter points to the bleak picture that the CEO painted of the company, all the while buying the stock behind the scenes while likely having material non-public information. Allowing the CEO to buy the company & even entertaining an offer below rejected bids would be a travesty for shareholder & they called upon the board to run a “real” process, free from his influence. They also pointed out that the board was rife with conflicts & allowing these so called ‘independent’ directors to be allowed part of the strategic committee was problematic.10

If Mr. Mizrahy wanted to own InMode, he could have competed in the open process like any other bidder. Instead, he watched where bids landed, let them die, bought stock for himself, enlisted the Company’s own manufacturer and distributor as partners, and now relies on a Board he plainly considers friendly, and which appears to be under his control, to wave it through. That he could expect such a reception is itself an indictment of this Board.

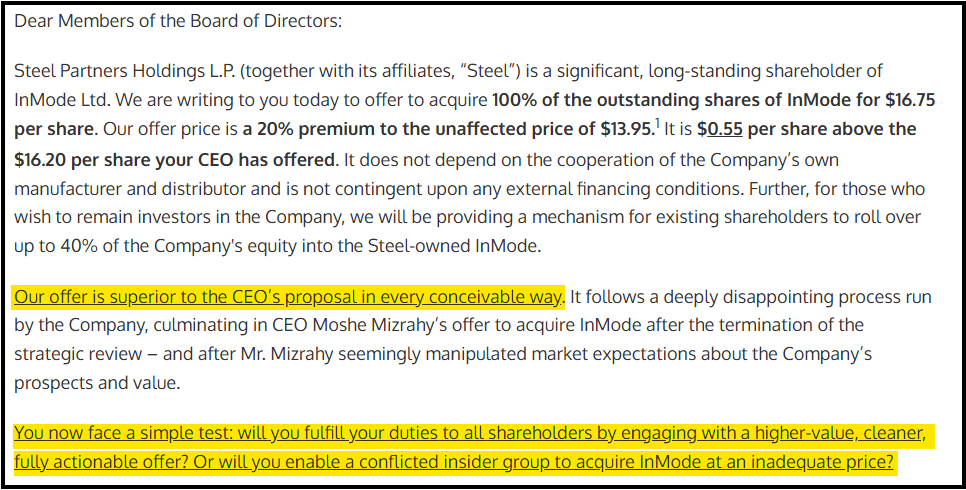

Steel Partners Offers $16.75 !

I was wrapping this post up & was pretty close to hitting send when the Steel Partners $16.75 bid came across the desk. They’ve bumped the CEO’s bid by $0.55 & offered a rollover option. Most importantly it calls out the board to do the right thing. 11

Steels paints a pretty damning picture of Mizrahy & hammers home the point of the CEO driving down earnings, making negative public comments about the company & then attempting to take advantage of the gap he has created.

The Summary

Ok, so I think the CEO has been purposely negative. I think a take private was always on the cards, but Steel forced the boards hand in Jan. The CEO thinks it’s his company & he managed to convince the board, the first time, that the offers, for whatever reason, weren’t good enough or couldn’t get across the finish line. Hence the “Keep InMode in Israel” comments.

But now Steel Partners & Doma have shone enough light on the situation that it will be very hard for the board not to look beholden to the CEO & not to approve the best proposal. Most importantly, this time, Steel bid for the whole company. That said, I find it hard to think that the CEO will let Steel Partners have this. Also, I don’t really think Steel Partners want it - as much as they need to force management to pay up. A management bump to $17 might even get it done - but that’s 10% more from here & a free look at a bidding war should things escalate. There’s also the possibility of a Korean conglomerate coming in over the top - as we know Centroid, a South Korean private equity firm were in the mix last time.

On Friday, in a 6-k InMode confirmed they received the acquisition proposal from Steel Partners & quietly noted that the expiration date of the CEOs proposal was extended until Sept 15th. All to play for here ! 12

Other Interesting Things…

Buybacks

Historically the company has bought back quite a bit of stock. From 2022 through 2025 they bought back 27.3m shares for $508m. However in early 2025 the CEO appeared to be frustrated with the stock price enough to stop buying back stock.

This stance changed in 2026 when they bought back ~$34m in the first quarter alone & $52.7m YTD through March 6th…… right around the same time the CEO was in the market.

Potential Violations of Securities Law / MNPI

Both Activists alluded to pretty serious governance concerns & more importantly potential insider trading alleging the CEO managed expectations down ahead of his own bid & that the ~800k share purchase comes awfully close to trading on material non-public information. The CEO may even have to get this done just to get out of the spotlight & the reach of the SEC.

Steel also pointed out something interesting & potentially damning for the board here, that the CEO offer was made on June 15th - three days before the AGM per the Proxy - yet there was no mention of the proposal in the AGM docs. This is definitely the sort of thing that ISS/ Glass Lewis will focus on when advising proxies.

Mr. Mizrahy drives the earnings down, inserts himself into what should be an independent strategic review and then comes back and reaches for the lowest number possible in order to steal the Company from its shareholders – the rightful owners. That is a clear breach of fiduciary duty and is one more reason he is no longer the right person to lead InMode.

Israeli Corporate Actions / Tax Considerations

Israeli withholding tax procedures can complicate how & when you receive the proceeds - so you may receive net & have to file a bunch of forms to get your wht back. Just something to note.

Razorblade Model

I find it hard to think of reasons why they haven’t pivoted to a razorblade model - where the initial machine purchase would be less & the recurring revenue would be driven by some sort of applicator sales. Perhaps its because their capex is low enough not to have to. But I don’t have a good answer. Perhaps that’s in the future & the CEO wants to own it outright first.

CTO

Michael Kreindel, the firms co-founder & CTO filed a 13D. He had never previously filed a 13D. He owns 3,114,762 shares / 5.11 % of the company. I would have to assume that he is in the buyout group - but he is not mentioned. Was he left out, so as to be able to vote (for management) as part of the minority ?

Brand Recognition / Celebrity

InMode has attracted some big celebrities in recent years with the likes of Kim Kardashian & Eva Longoria endorsing the products. Should any of their newer products gain organic celebrity endorsement, sales could quickly climb.

The Disclaimer(s)

Disclaimer #1: You should know by now, I am Jon Snow, I know nothing. I could be & probably am, missing a bunch of reasons why this doesn’t work.

Disclaimer #2: As always, please, if in any doubt, please refer to disclaimer #1, I am Jon Snow. I know absolutely less than nothing. Don’t listen to me. In fact, put all your money into an index fund & laugh at the rest of us. I make mistakes, lots of them, in fact. Please feel free to point out if, or how many, I may have made above.

Disclaimer #3 : This commentary is for informational & personal opinion purposes only. IT IS NOT FINANCIAL ADVICE ! (let’s face it, it’s basically comedy), and I am not your fiduciary. You should do your own research and consult a qualified financial advisor before making any investment decisions. DYODD !! & DO NOT TAKE INVESTMENT ADVISE FROM PEOPLE ON THE INTERNETS THAT FOUND INVESTMENT RELIGION DURING COVID … or me for that matter !! I may buy or sell at any time…. most likely the day before a Korean buyer pays an uneconomical price of $19. You do you.

https://www.nasdaq.com/press-release/steel-partners-holdings-lp-announces-it-has-presented-1800-share-offer-51-inmode-ltd

https://www.sec.gov/Archives/edgar/data/1742692/000117891326000268/exhibit_99-1.htm

https://en.globes.co.il/en/article-keep-inmode-in-israel-1001533596

https://www.sec.gov/Archives/edgar/data/1742692/000117891326000583/exhibit_99-1.htm

https://www.sec.gov/Archives/edgar/data/1742692/000117891326002041/xslSCHEDULE_13D_X02/primary_doc.xml

https://www.sec.gov/Archives/edgar/data/1742692/000117891326002039/xslSCHEDULE_13D_X02/primary_doc.xml

https://www.sec.gov/Archives/edgar/data/1742692/000119312526280387/xslSCHEDULE_13D_X02/primary_doc.xml

https://www.sec.gov/Archives/edgar/data/1742692/000119312526280387/ck0001068238-ex99_1.pdf

https://www.prnewswire.com/news-releases/doma-perpetual-capital-management-strongly-opposes-inmode-buyout-as-proposed-plans-to-vote-against-deal-302811416.html

https://www.businesswire.com/news/home/20260629203388/en/Steel-Partners-Holdings-L.P.-Issues-Letter-to-InMode-Ltd.-Board-of-Directors-Highlighting-Serious-Concerns-with-Value-Destructive-CEO-Led-Buyout-Proposal

https://www.businesswire.com/news/home/20260709185983/en/Steel-Partners-Offers-to-Acquire-InMode-for-%2416.75-Per-Share-in-Cash

https://www.sec.gov/Archives/edgar/data/1742692/000117891326003456/zk2635669.htm